The scale of the market that liquidity aggregation serves continues to grow:

Liquidity aggregation pulls price feeds from multiple LPs simultaneously: banks, exchanges, and prime brokers.

The engine manages the following continuously:

When a client places an order, the engine processes it in sequence:

Liquidity aggregation serves two main purposes:

In live trading, LPs experience outages, connectivity drops, or stop sending quotes without warning. There are two types of failover scenarios a broker may encounter:

In both cases, the failover logic works both ways. The liquidity aggregator not only switches away from a failing provider or symbol feed, but automatically switches back once the primary source is restored.

Aggregating liquidity from multiple sources improves trading conditions across several dimensions: pricing, market coverage, execution speed, counterparty risk, and instrument availability.

The entire order is routed to a single liquidity provider — the one offering the best price, or the top provider on a priority list.

Volume is split across multiple LPs and their price levels, so the client receives a blended price reflecting the best available liquidity across sources. Behavior differs by order type: IOC (Immediate-or-Cancel) orders can be divided across several levels and providers, while FOK (Fill-or-Kill) orders are matched only against the top of book, with no splitting.

This is a configuration available within advanced aggregation: fixed percentage splits for specific LPs, with any remaining volume distributed according to standard advanced-aggregation logic.

This is a behavior worth flagging in advanced aggregation: the closing leg of a trade is re-evaluated against the live book at the time of close, and may execute with a different provider than the one that opened it. Partial closes can also leave residual volume open with the original provider.

More LPs do not guarantee better fills for clients. In fact, two or three providers are often sufficient to ensure effective risk management and client satisfaction. Let us consider the main types of liquidity providers in the market.

These liquidity sources can be categorized based on their role in the market, their level of liquidity, and the execution models they support.

Real-time data processing is essential for ensuring seamless trade execution and price discovery. The aggregation process involves collecting, analyzing, and distributing vast amounts of financial data from multiple liquidity providers. To maintain efficiency, systems must process this data with minimal latency, ensuring that traders receive the most accurate and up-to-date pricing information. High-speed data processing infrastructure helps liquidity aggregators dynamically adjust orders, minimize slippage, and improve trade execution quality.

One of the key challenges in real-time data processing is managing the high-frequency data streams coming from different liquidity sources. These streams must be normalized and synchronized to ensure consistency in pricing and trade execution. Technologies such as distributed computing, in-memory data grids, and parallel processing are often employed to handle these massive data flows.

By leveraging these solutions, liquidity aggregators can maintain a real-time view of the market and respond instantly to fluctuations, reducing the risk of outdated price information affecting trade execution.

Low-latency networking is a fundamental requirement in real-time liquidity aggregation. In financial markets, where prices fluctuate within milliseconds, even the smallest delays in processing liquidity data can lead to missed trading opportunities, increased slippage, and higher trading costs. To mitigate this, liquidity aggregators employ ultra-low-latency systems that can capture, process, and transmit data in real time. This requires not only high-speed hardware, such as field-programmable gate arrays (FPGAs) and graphics processing units (GPUs), but also specialized software optimizations that reduce computational overhead.

To further enhance low-latency execution, liquidity providers and trading firms utilize co-location services, where their servers are physically placed near exchange data centers. By reducing the physical distance between trading infrastructure and exchange matching engines, co-location can cut down network transmission times to microseconds.

Additionally, financial institutions leverage cutting-edge networking protocols like FIX (Financial Information eXchange), WebSockets, and proprietary high-speed messaging systems to ensure orders and market data updates are transmitted with minimal lag.

Moreover, the rise of edge computing is bringing liquidity aggregation closer to the source. Instead of sending data to centralized cloud servers, edge computing allows liquidity data to be processed at distributed nodes closer to exchanges and liquidity providers. This significantly reduces the time required to analyze and act on market changes, improving execution speed.

Alongside this, advanced AI-driven predictive models are being used to anticipate price movements and execute trades milliseconds ahead of competitors, further enhancing liquidity efficiency.

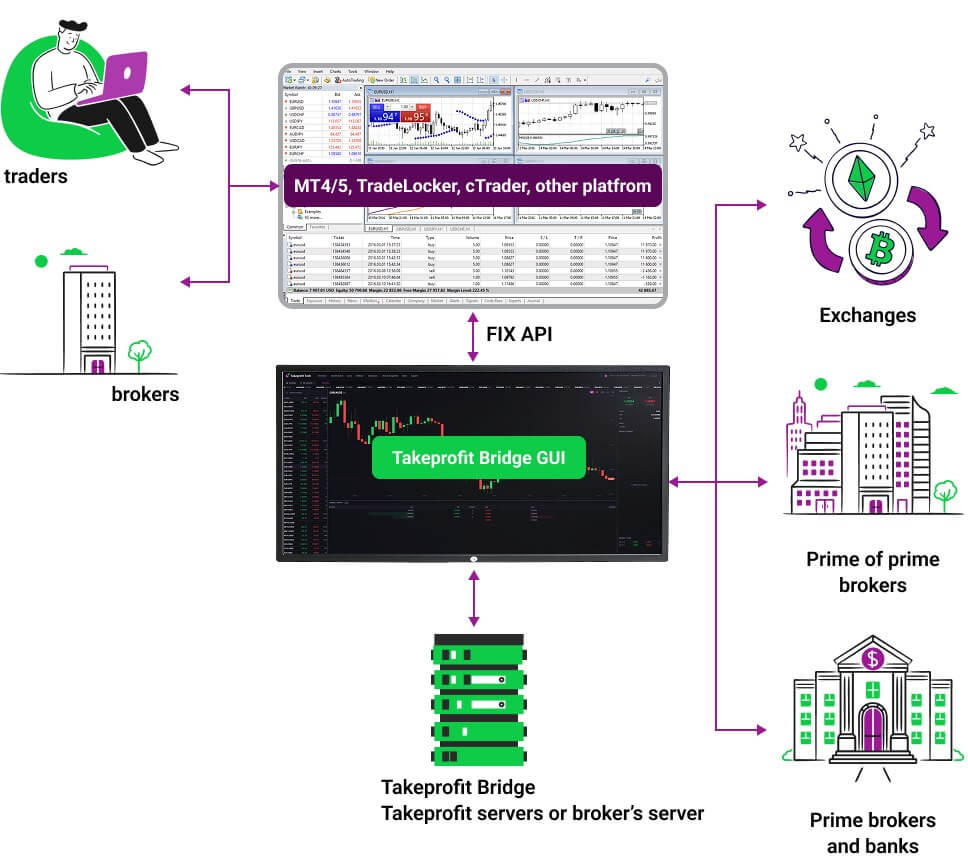

Liquidity aggregators, such as Takeprofit Bridge, allow brokers to automate risk management and seamlessly aggregate liquidity from multiple providers.

While both retail and institutional brokers use liquidity aggregators, they do it in different ways. Institutional brokers distribute liquidity to smaller brokers, ensuring efficient market access.

Meanwhile, retail brokers use aggregators to manage liquidity across their trading platforms, where transactions are executed directly.

In highly regulated jurisdictions, brokers offering CFDs or leveraged FX to retail clients are subject to strict best execution, conduct, disclosure, product governance, client money, and conflict-of-interest requirements.

As a result, many regulated brokers use A-book, STP, or hybrid execution models supported by liquidity aggregation to improve price discovery, benchmark execution quality, manage risk, and maintain a more auditable execution framework.

Some offshore and international financial centres generally provide brokers with more flexibility in choosing their execution model compared with Tier 1 jurisdictions. However, this should not be described as the absence of regulation.

Offshore flexibility can make execution-model design easier, but it may also limit access to some regulated, institutional-grade liquidity providers, banks, and payment partners that apply stricter onboarding and due diligence standards.

Modern aggregation solutions are technically mature, but the environment they operate in continues to create new pressures. Several structural challenges affect brokers and liquidity providers alike.

Liquidity aggregation is expected to become increasingly important as financial markets grow more fragmented, automated, and data-driven. As traders interact with more exchanges, liquidity providers, ECNs, market makers, OTC desks, and decentralized platforms, the ability to connect these sources into one unified liquidity pool will become a competitive advantage.

One of the strongest drivers behind liquidity aggregation is the continued growth of trading volumes across global markets. According to the Bank for International Settlements, daily OTC foreign exchange turnover reached $9.6 trillion in April 2025, up from $7.5 trillion three years earlier, showing a 28% increase in global FX activity. This growth highlights why brokers, banks, and trading platforms need more advanced systems to access liquidity efficiently across multiple venues.

As market activity increases, liquidity is not always concentrated in one place. According to FESE’s 2025 report on European equity markets, liquidity fragmentation remains a key issue, especially within individual markets, where trading activity is spread across competing venues. The report argues that reducing fragmentation could help unlock deeper liquidity and improve market efficiency.

Another major trend is the use of artificial intelligence and machine learning in liquidity aggregation. Instead of simply routing orders to the venue with the best visible price, future systems will evaluate execution speed, historical fill rates, market depth, volatility, latency, and counterparty reliability in real time.

This trend is closely connected to the broader growth of algorithmic trading. According to Grand View Research, the global algorithmic trading market was valued at $21.06 billion in 2024 and is projected to reach $42.99 billion by 2030, growing at a 12.9% CAGR from 2025 to 2030. This suggests that automated execution technologies, including smart order routing and liquidity aggregation, will play a larger role in modern trading infrastructure.

The FX market is likely to remain one of the most important areas for liquidity aggregation. According to Growth Market Reports, the global FX liquidity aggregation market reached $1.45 billion in 2024 and is expected to grow to $3.21 billion by 2033, with a projected 9.2% CAGR from 2025 to 2033. The report links this growth to rising demand for real-time pricing, better transparency, and more efficient execution in volatile currency markets.

For brokers and institutional traders, this means liquidity aggregation will no longer be just a technical feature. It will become a core part of execution quality, pricing competitiveness, and client retention.

Liquidity aggregation is also expected to expand in digital asset markets. Crypto liquidity is often spread across centralized exchanges, decentralized exchanges, OTC desks, market makers, and blockchain-based liquidity pools. This creates a need for systems that can combine liquidity from different sources while managing execution risk, price impact, and settlement complexity.

According to TokenInsight’s 2025 crypto exchange report, institutional legitimacy, operational resilience, and derivatives trading became major themes for crypto exchanges in 2025. This supports the idea that more professional market infrastructure will be needed as digital asset trading matures.

Regulation will also influence how liquidity aggregation develops. As financial authorities focus more on best execution, transparency, and market stability, aggregation platforms may need stronger reporting tools, audit trails, and risk controls. This will be especially important for brokers and financial institutions operating across multiple jurisdictions.

In the long term, liquidity aggregators that combine broad market access with compliance-ready infrastructure are likely to gain an advantage. Traders will not only expect better pricing, but also clearer execution data and proof that orders are routed in the most efficient way possible.

Overall, the future of liquidity aggregation points toward smarter routing, wider market connectivity, and greater transparency. Rising FX volumes, the growth of algorithmic trading, and continued market fragmentation all show that demand for advanced aggregation technology is likely to increase. For brokers, exchanges, and institutional traders, liquidity aggregation will become essential for reducing slippage, improving execution quality, and accessing deeper liquidity across an increasingly complex global market.

Ekaterina Nutriakova

Ekaterina Nutriakova